Raw Material Supply Chains in the Transition to Low-Carbon Steel: The Critical Role of Strategic Cooperation Between DRI Projects and Iron Ore Producers

In his analysis of the news about the completion of POSCO’s largest electric arc furnace in Gwangyang, Dr. Bararzadeh describes the project not merely as an industrial investment, but as a turning point in the structural transition of South Korea’s steel industry toward low-carbon production and as a foundation for hydrogen-based steelmaking.

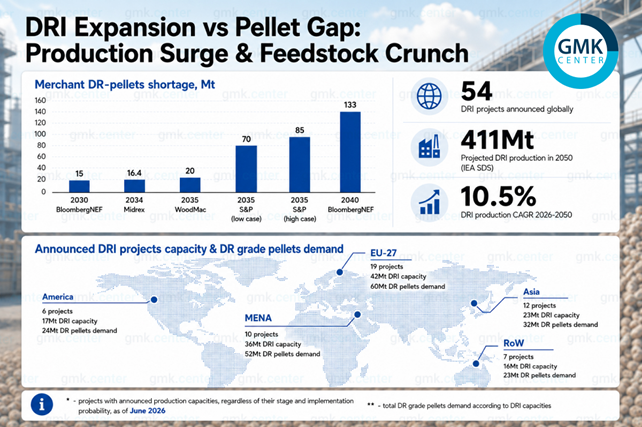

In recent years, the steel industry’s transition toward carbon-emission reduction has evolved from a purely technological issue into a deeply supply-chain-driven and structural challenge. In this context, direct reduced iron technology has emerged as the main pathway for low-carbon steel production worldwide. However, the development of this pathway depends less on production capacity itself and more on stable access to suitable raw materials. This dependency has become a key bottleneck in the global steel transition, particularly with regard to high-grade, or DR-grade, iron ore.

scale projects with capacities of tens of millions of tons are either being planned or implemented. This rapid growth reflects a paradigm shift in the steel industry, but at the same time it is placing increasing pressure on the global iron ore market and turning the sustainable supply of feedstock into a strategic challenge.

From a geographical perspective, the distribution of these projects is uneven, and different regions of the world play different roles in the low-carbon steel value chain based on their energy advantages and mineral resources. In some regions, such as Europe and the Middle East and North Africa, the development of direct reduced iron projects is largely based on imported iron ore. This increases dependence on global markets and sensitivity to fluctuations in seaborne trade. By contrast, countries such as Australia, Brazil, and the United States benefit from direct access to iron ore resources and low-cost energy, giving them a different competitive position.

In recent years, iron ore quality has become one of the most important structural constraints on the development of low-carbon steel. Direct reduction technology requires feedstock with high iron content and specific metallurgical properties, and this type of iron ore represents only a limited share of global reserves. Industry estimates indicate that the future demand of announced direct reduced iron projects for DR-grade pellets will increase significantly, while the share of tradable supply available in the open market accounts for only a small portion of total global production. This imbalance between supply and demand points to the emergence of long-term structural pressure in the raw materials market.

Various forecasts also confirm this concern, indicating the possibility of a significant supply deficit in iron ore suitable for low-carbon steel production over the coming decades. This supply gap is expected to persist not only in the short term but also over longer horizons, potentially becoming one of the main barriers to the development of direct reduction technologies.

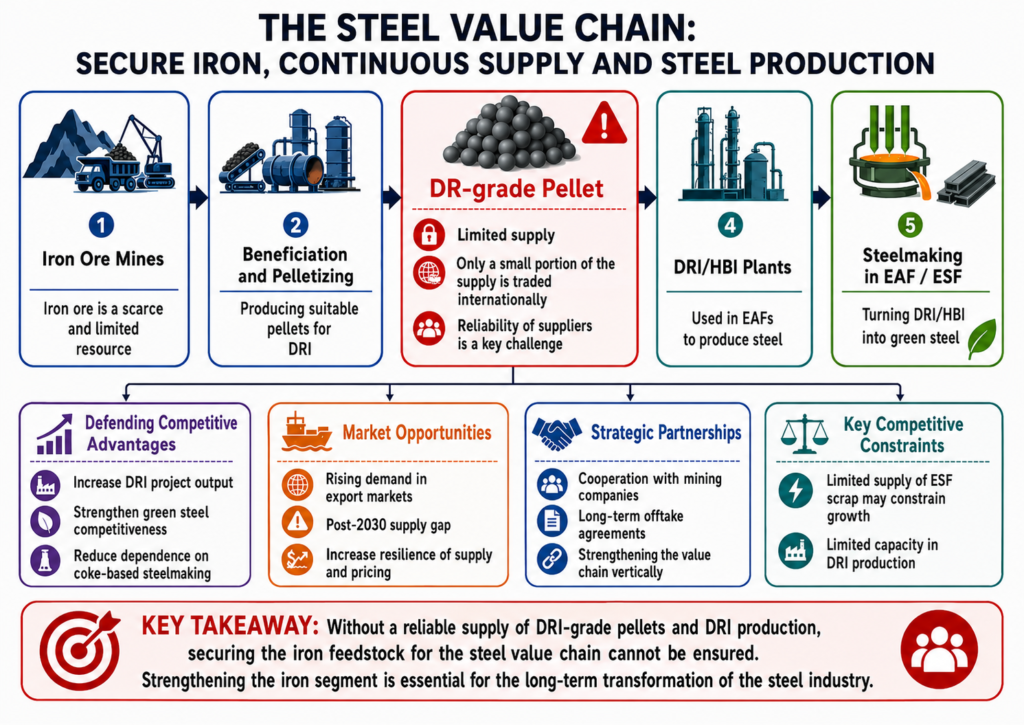

Meanwhile, some technical solutions, such as the use of electric smelting furnaces as a complement to direct reduction technology, have been proposed. However, these options can only partially ease the constraints and cannot fully resolve the global shortage of raw materials. The limited global production capacity of suitable pellets also shows that, despite technological progress, feedstock supply will remain a serious challenge.

Accordingly, the future success of direct reduced iron projects will depend more than ever on the formation of long-term, strategic cooperation between steel producers and mining companies. Such cooperation may take the form of stable supply agreements, vertical integration across the value chain, or joint investments in iron ore mines. In the absence of such partnerships, the risk that raw material constraints become the main bottleneck in the transition to low-carbon steel will increase significantly, potentially slowing the structural transformation of the global steel industry.